04.17.2026

The Spec Economy

How East Asia's development model built world-beating factories, mediocre websites, and endless confusion in the West

I grew up in the middle of the Hsinchu Science Park, a 15-square-kilometer plot carved out of tea fields and sugarcane plantations in northern Taiwan.

The experience of growing up there was particularly anodyne. Other than the fabs and office buildings scattered across the area, the Science Park was mostly mid-rise company apartments, neat sidewalks, reasonably well-kept trees, and not much else. Compared with the usual chaos and mixed-use vibrancy of urban Taiwan, it felt almost suburban. For a teenager, it was pretty boring.

We lived in a strange bilingual bubble: JanSport backpacks, American accents, prom, and ‘Party in the U.S.A.’ on one side; school cleaning duties and memorizing Classical Chinese poetry on the other. Most of us were returnees from the United States or Canada. Somewhere around 70 to 80 percent had at least one parent in semiconductors or academia.

What struck me, even as a child, was how clearly you could see where our world ended and the rest of Taiwan began. There was a literal physical line between the internationally competitive, high-tech face of the country and the local economy outside it, sprawling more organically toward the city center.

As the world has belatedly discovered over the past few years, this modest patch of land also sits at the center of one of the most strategically important industrial clusters in the world. TSMC alone fabricates the chips that power everything from iPhones to AI accelerators to a large share of America’s precision-guided weapons. Taken together, the major listed semiconductor firms in and around Hsinchu account for well over $2 trillion in market capitalization.

And yet if you actually lived in Hsinchu, you knew that receiving a wire transfer from abroad could still mean driving ten minutes to a local branch, taking a number, sitting on a creaky plastic chair, and watching someone process your transaction on what looked like a computer from another era. Then came the personal stamp, the two forms of photo ID, and another half hour signing forms containing information that surely already existed somewhere in the system.

As a child, this all seemed normal. As an adult, this was downright bizarre.

How could a society capable of nanometer-scale manufacturing at inhuman yields still struggle to modernize ordinary parts of everyday life? Why could Taiwan figure out one of the hardest industrial processes in the world, but not a decent banking interface?

Taiwan is not unique - versions of this dissonance show up across East Asia.

Spend enough time in or around Japan, Korea, Hong Kong, China, or even Singapore and the same contradictions and complaints quickly appear (often on Reddit). From a distance these places can look safe, coordinated, clean, and technically formidable in ways much of the contemporary West seems to have forgotten.

Up close, they can be inexplicably archaic in software, administration, banking, retail systems, and all sorts of mundane customer experiences.

That contradiction becomes even stranger once you zoom out. In an era of industrial-policy panic and renewed geopolitical competition, East Asia does not merely feel formidable. In sector after sector, it is overwhelmingly dominant:[1]

| Product / category | Country | Global market share |

|---|---|---|

| PV wafers | China | 95% |

| Battery anode active materials | China | 97% |

| Lithium-ion battery cells | China | 85% |

| Rare-earth separation / refining for magnet REEs | China | 91% |

| NdFeB permanent magnets | China | 94% |

| Shipbuilding | China + South Korea + Japan | ~90-95% (China: 50-54%, South Korea 25-30%, Japan: 10-15%) |

| Sub-7nm logic foundry | Taiwan | >90% |

| Notebook computers | Taiwan | 74.3% |

| Data center / AI servers | Taiwan | 80%-90% |

| DRAM | South Korea | ~68% |

| HBM | South Korea | ~78% |

| Semiconductor coaters / developers | Japan | 88% |

| Silicon wafers | Japan | 53% |

| Photoresists | Japan | 50% |

Sources: IEA (ETP 2026, Global EV Outlook 2025); UNCTAD (Review of Maritime Transport 2024); USITC (U.S. Exposure to the Taiwanese Semiconductor Industry); TrendForce; U.S. Department of Commerce; Reuters ↩︎

These numbers send policymakers, industrial strategists, and a certain genre of venture capitalist into a cold sweat. They also send many people grasping for explanations. A lot of those explanations reach for sweeping cultural or essentialist claims - they are not always wrong as surface-level description, but they collapse on contact with the historical record and social changes.

The better explanation is structural: the same development model pioneered by Japan and adopted across much of Asia produced both its world-leading strengths and many of its everyday frustrations.

The mechanism

The core approach of the East Asian development model isn't a mystery: Japan, then the newly industrializing economies, used manufacturing exports as a way to convert cheap labor, scarce capital, foreign technology, and American market access into industrial capability.

Unlike the more domestic-oriented consumer markets that Western Europe leaned on as they recovered from the war, most of East Asia stepped out of the ruins of World War II by selling into buyers eager for manufactured goods. Textiles, garments, toys, wigs, plywood, and light assembly - then steadily moving up the value chain into steel, ships, electronics, automobiles, semiconductors, displays, batteries, and advanced industrial components that firmly established each as an industrial power in turn.

Key industries where absorbing foreign technology was desirable were protected by import-substitution and tariffs to build competencies and an industrial base. Firms were geared towards integrating into the global supply chain and building to someone else's specification.

Like water, economies flow towards the path of least resistance. If a country is blessed with plentiful commodities and resources, it will build an economy around that. If it starts with beautiful beaches, it will build a tourism industry. East Asian economies with not a lot of resources, a lot of people, and access to U.S. and Western markets in a multi-decade run of trade liberalization, rolled up their sleeves and got to building and copying industrial products.

Japan rebuilt through steel, shipbuilding, automobiles, consumer electronics, industrial machinery, and eventually a dense ecosystem of precision components, semiconductor equipment, and materials. Korea came up through wigs (!), plywood, garments, then heavy industry and electronics. Taiwan moved from textiles and cheap manufacturing - at some point dominating 70-80% of the global umbrella market - into contract electronics and then semiconductors.

In the case of Taiwan, ASUS started as an OEM/ODM. HTC was originally an ODM making phones for carriers — in fact, the first ODM for Android phones. Foxconn has held the crown for the world's largest electronics manufacturer for almost two decades:

The phrase that best captures this mode is building to spec.

Someone else — usually a Western brand or systems integrator — decides what the product should do, what it should look like, what it should cost, and how it should be sold. You build it. Your job is to hit the spec, hit the deadline, hit yield, and do it more cheaply and reliably than anyone else. This model, more so than any other, rewards variance reduction — generating predictable outcomes.

Doing this in the context of modern manufacturing at the frontier of technology demands a very specific kind of organization: people trained to shave defects down to parts per billion, hold tolerances in the nanometers, and keep just-in-time global supply chains from snapping at the weakest link.

As a result, the societies that have mastered this have built up an enormous, durable stack of capabilities: process discipline, yield engineering, materials science, supplier coordination, capital deployment at scale, and client management.

It bears noting what this model doesn’t need and actively suppresses: it doesn't require a firm to be able to figure out what the product should be or to speculate over what the user might be delighted by. It doesn't reward the kind of organizational slack that permits hundreds of junior employees to spend 20 percent of their time experimenting with promising moonshot projects.

Firms organized around hitting someone else’s spec get extraordinarily good at hitting specs. They do not, by the same process, get equally good at exploring product concepts the world yet know they want.

If they want to do this, these societies will have to develop other champions with different incentives and organizational structures to achieve that.

The Dual Economy

Economists have long described developing countries as "dual economies" — W. Arthur Lewis's 1954 formulation was about farms versus factories — but what I'm pointing at is a later, more confusing version: two modern sectors inside the same country, one world-class and one visibly not.

On one side sits the internationally exposed export sector: the fabs, factories, engineers, industrial ministries, capital-allocation systems, and elite firms plugged into brutal global competition. This is the side outsiders see when they visit Shenzhen, tour Toyota plants, or marvel at TSMC: the side of the economy exposed to global competition and customers.

On the other side sits much of the domestic economy: local services, banking, administration, retail systems, small firms, and the broader mass of non-tradable sectors that do not face the same pressure — they don’t have to be world-class.

I hope I don't need to convince you that East Asia isn't inherently deficient in intelligence, ambition, or creativity.

What the current state of affairs does mean is that the incentive structure pointed talent development, capital, prestige, and policy attention toward the export machine. Nobody needed Taiwanese SMEs to have great software, or local banks to offer elegant digital experiences, in order for the country to win the next Apple contract or the next process-node race. The domestic economy was structurally much less important to success abroad.

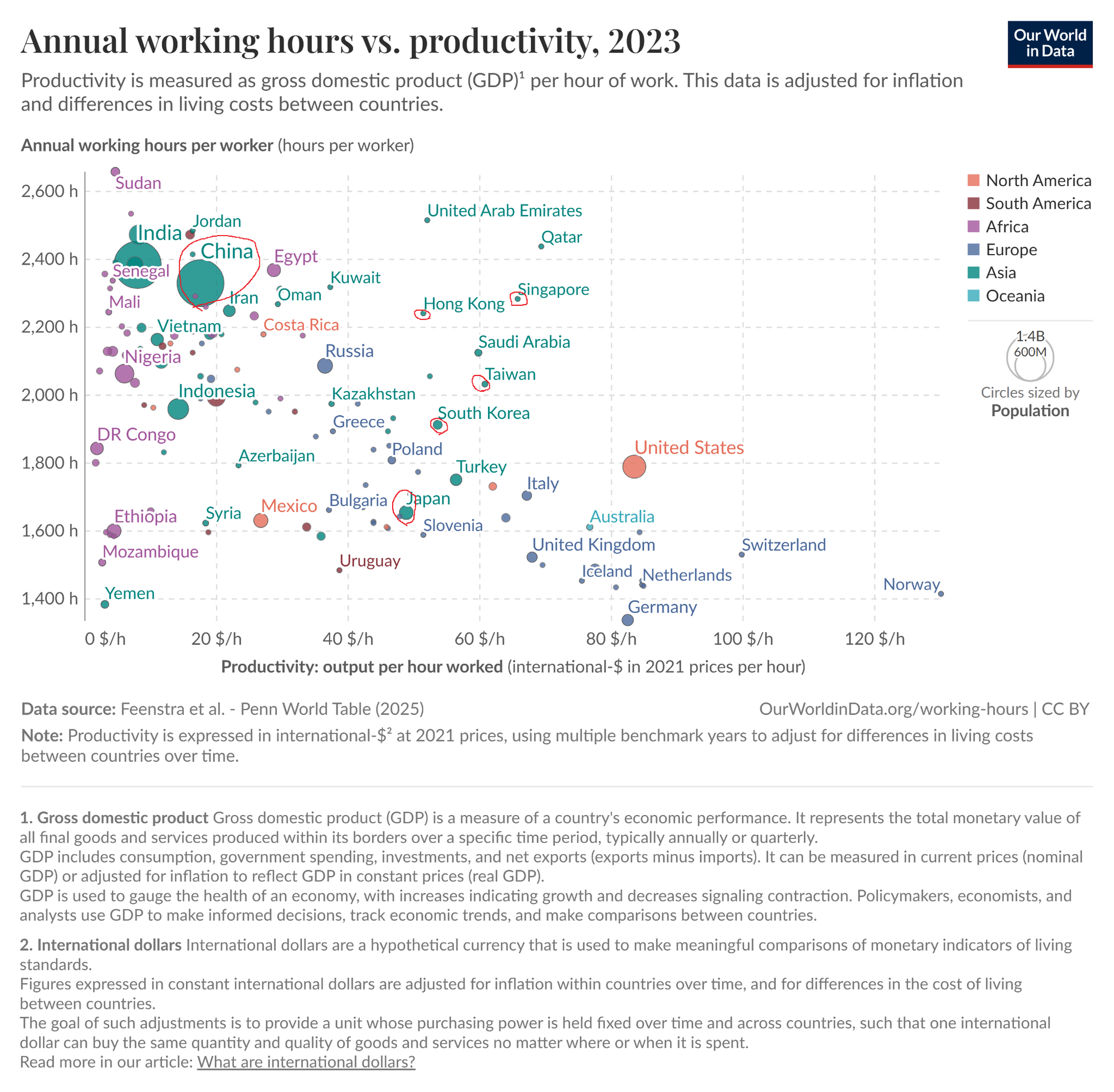

The result is a major drag on overall labor productivity. Some gap between manufacturing and services is universal and expected — this is Baumol's cost disease, the observation that services (a haircut, a therapy session, a classroom lecture) resist the productivity gains that transform manufacturing.

What's striking here is that Korea's service sector labor productivity is only 44% of manufacturing, compared to the OECD average of 84%. In the decade from 2013-2022, Korea's manufacturing productivity grew 19% while services managed just 6%, and SME productivity in services actually declined.

In 2008, Japan ranked 3rd among OECD countries in manufacturing productivity while ranking 19th overall: the gap between those two numbers is the dual economy. By 2026, Japan has since fallen to 29th overall and continues to drop. Even in China, where the gap is smaller, industrial productivity runs about 30% higher than services and the differential is widening as workers shift from factory floors to low-skill service jobs.

The dual economy in Asia isn't just Baumol's gap: it's Baumol's gap on steroids.

The pattern becomes hard to miss once you look at cross-country comparative data - which is somewhat shocking. Even most advanced Asian economies are somewhat middling here, achieving something between 60-80% of the labor productivity of Western countries. I think few people expect labor productivity to be higher in Italy than in Singapore.

What's interesting here is that Poland and the Czech Republic have been following a similar catch-up path through export manufacturing and integration into Western European supply chains. The vehicle has differed — more greenfield investment and foreign ownership, less indigenous contract manufacturing — but the shape is highly recognizable: strong export sectors, weaker domestic productivity, and relatively few globally dominant homegrown consumer brands.

Not to overextend the idea, but Poland tied with Japan for 4th place in the 2025 International Mathematical Olympiad and has a fertility rate of 1.1.

Suspiciously "Asian."

Any society that routes its best engineers into process improvement, manufacturing yield, supplier management, and examination pathways will produce a lot of people who are extremely good at those things. A society that routes its best technical talent into venture-backed software, product management, speculative consumer markets, and winner-take-most platforms will produce a different kind of technical culture.

Where Polish-founded software startups have succeeded globally - like recently with ElevenLabs - it has inevitably required setting up shop elsewhere in more fertile locales.

Succeeding is not impossible, of course. East Asia has already produced extraordinary consumer companies, brands, platforms, and cultural exports. Japan gave the world Sony, Nintendo, Toyota, Muji, Uniqlo, and Studio Ghibli. Korea gave the world Samsung, Hyundai, LG, K-pop, K-drama, beauty, and consumer electronics with real global pull. China has produced DJI, BYD, ByteDance, Xiaomi, Huawei, and a digital consumer ecosystem that in some areas leapfrogged the West. Taiwan has world-class hardware and semiconductor firms, even if its consumer internet sector is much less impressive than its fabs.

But how much of this is a) building in areas where variance-reduction itself drives outsized competitive value, b) capturing value in proven markets, and c) succeeding despite the environment, instead of because of it?

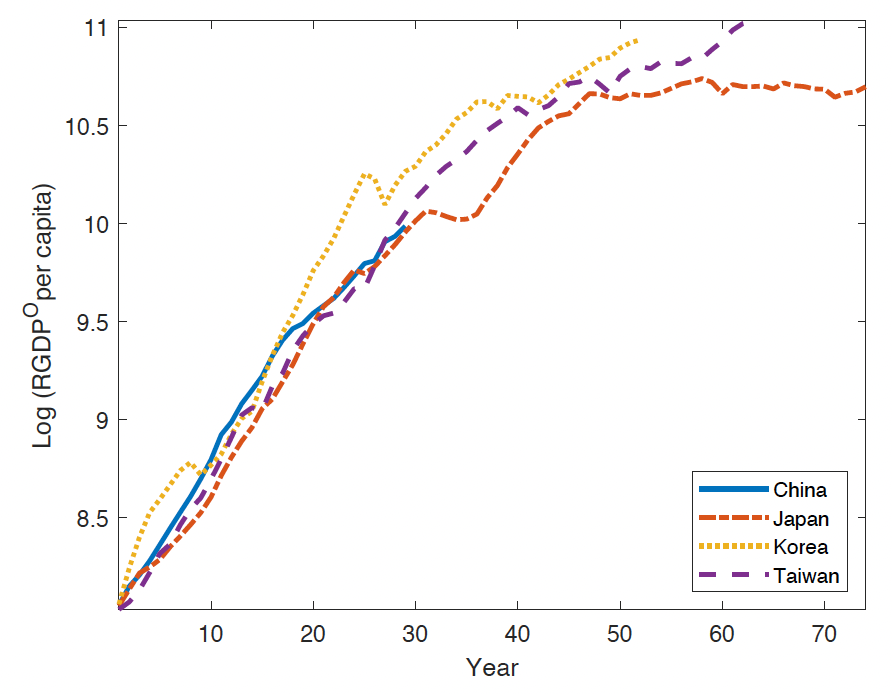

A recent economics paper by Jesús Fernández-Villaverde, Lee Ohanian, and Wen Yao that I came across earlier this year mapped out China’s long-run growth path compared to previous East Asian economic miracle stories, approaching this with a relatively simple approach: start with a baseline economic growth model, add data around total factor productivity (TFP) catch-up, and see where that led:

Every economy in the sample tracks the same arc, and every one hits the same ceiling around the same relative income level. It’s easy to group all of these nations together because of proximity and race, but they differ enormously in size, scale, politics, and culture.

I would argue that the familiar pattern of rapid early catch-up followed by a bottleneck driven in large part by this dual-economy structure and developmental model. The export sector drives the miracle years. Later, the underperformance of domestic services, weak consumer-facing innovation, and slower diffusion of productivity gains become harder to ignore.

Where an economy appears to break past the bottleneck, as Taiwan recently has with blistering fast annual GDP growth above 8.6% in 2025, it is often because the export machine is so large relative to the rest of the economy that it can pull aggregate numbers upward almost by itself. Most East Asian economies are too large for a single export sector to do that — and reliance on a single sector for growth can be brittle.

If an economy rewards people for producing to spec and crushing variance, its schools and workplaces will tend to reward the same traits: exam performance, hierarchy navigation, loyalty, and disciplined execution inside tightly coordinated systems.

At the core of the paradox: to the outside observer, Asia can look futuristic, hyper-competent, and somehow wielding terrifying industrial might. From the inside, it can feel oddly clunky, hierarchical, and behind in all sorts of ordinary consumer experiences. Those are not contradictory impressions - they are two sides of the same development model, and one that goes well beyond East Asia.