05.04.2026

Atoms to Bits and Bits to Atoms

Why East Asia struggled with VC-backed startups, and why AI is making the region’s industrial inheritance matter again

One of the conundrums that I’ve been exploring over the last few years is why the success of venture capital and startups seems to have been comparatively modest in East Asia. Normalized for GDP and population, the largest East Asian countries compare to the U.S. as follows:

Sources: Crunchbase via Visual Capitalist, July 2025; IMF 2025 nominal GDP; CIA World Factbook / World Bank population.

Japan’s numbers are extremely underwhelming relative to its industrial sophistication and large economy of close to $5 trillion. South Korea looks better, but is still underpowered for a country that was able to produce highly competitive global tech conglomerates like Samsung, SK Hynix, Hyundai, LG, not to mention some of the most successful pop-culture exports of the 2010s and 2020s.

Even China – the peer competitor to the U.S. with innovation hubs like Beijing, Hangzhou, and Shenzhen, in a country boasting over a billion people, world-beating patent filings, and enormous scale – does not seem to be particularly exceptional when compared against its neighbors.

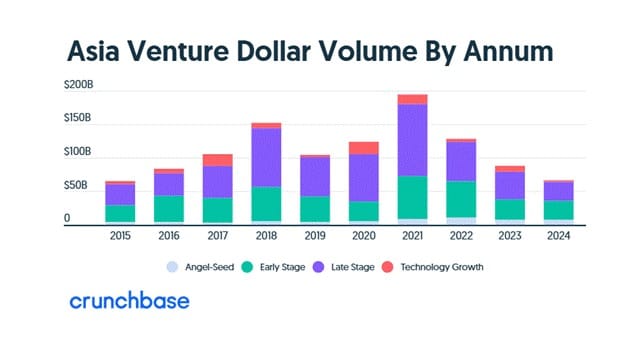

Even worse, the amount of venture capital invested in the region has been falling: Asia-based startup funding has fallen by 66 percent from a 2021 peak of $194 billion to $65.8 billion in 2024 – a 10-year low. This has been pretty universal: even in China, the amount of VC fell by 71 percent between 2021 and 2025.

This collapse in funding had multiple drivers: based on conversations that I’ve had with fund managers, part of this is due to capital moving out of other areas and flooding into the AI boom centered around San Francisco – close to 55% of VC investment globally in 2025 was directed towards SF Bay Area tech startups.

Simultaneously, the end of ZIRP has also compressed tech multiples and closed IPO windows. Thirdly, large swaths of Asia – especially Southeast Asia – were more deeply exposed to the 2021 growth equity bubble and have been suffering from a hangover from the draw down.

Ultimately, however, there is a sentiment that venture investing into software startups has been tricky to figure out in Asia – there have been a smattering of blockbuster hits across the region like Alibaba ($168B IPO), Coupang ($60B IPO), Xiaomi ($54B IPO), and Grab ($40B SPAC) – but big hits beyond e-commerce, local services like ride hailing and delivery, payments, and short video have been hard to come by.

There are vanishingly few true global software successes that have come out of Asia – a region with tens of millions of computer programmers, some of the world’s largest companies, and billions of people. Why?

The platform era and its evolution

Whether consciously or not, Silicon Valley – and the U.S. tech industry as a whole – had a comfortable arrangement with Asia. Taiwan would fabricate chips. Korea would make displays. Japan would supply specialized components. China would assemble the end product. California would package the result as products, ecosystems, platforms, and global brands – the top of the value pyramid, where the margins lived.

The idea here is that American companies would own the software, the platforms, the user relationships, and therefore the points of greatest leverage.

At the firm level, this was undeniably the right thing to do. Manufacturing was very clearly the lower level of the stack: labor intensive, pollution creating, commoditized and was paired with terrible compressing margins. The valuable work was happening upstairs, in offices equipped with kombucha taps and ping pong tables.

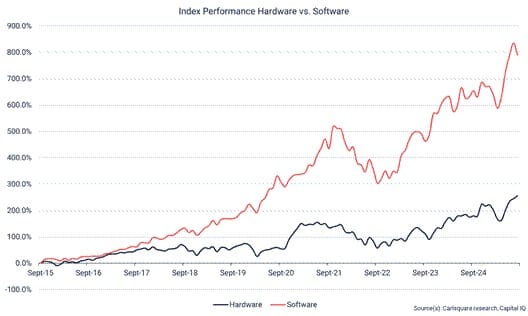

From 2015 to 2025, software companies outperformed hardware companies by more than 4x in public markets:

And the very biggest software companies pulled away from the rest of the market entirely. Aggregation effects produced winner-take-all dynamics that compounded into effectively a separate stock market (quite literally, with robust secondary markets providing liquidity today to tech startups) – right-tail outcomes that dovetail perfectly into justifying venture capital as a high-risk, high-return financing approach:

OpenAI’s launch of ChatGPT on November 30, 2022 and subsequent firestorm of interest seemed like very much of a continuation of the trend – the latest step change acceleration in software eating the world, with both OpenAI and Anthropic hitting close to trillion-dollar valuations and a flurry of unicorns of all sorts springing up across the value.

What is different this time, however, has been the massive inflection in demand for compute and everything that comprises it – packaging, fabs, high-bandwidth memory, grid transformers, grid connections, cooling, copper, batteries, sensors, nuclear power, gas turbines, land.

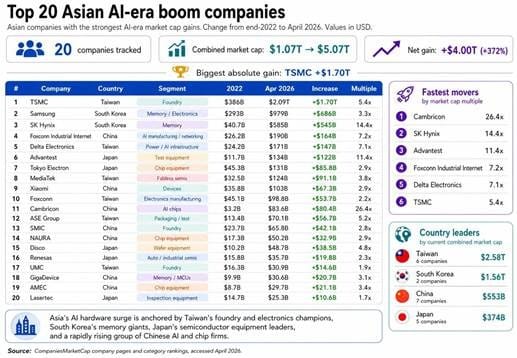

If we look at a basket of 20 Asian hardware companies, we see $4 trillion in market capitalization added. TSMC alone added $1.7 trillion. Samsung added $686 billion. SK Hynix, $545 billion in the last three-and-a-half years.

Capability Ladders

To understand how big this inversion was, look at the world’s twenty largest companies, then and now:

In 1989, thirteen of the twenty largest companies in the world were Japanese. Industrial banks, electric utilities, electronics conglomerates, steel mills – the East Asian developmental model at peak capital. Thirty-four years later, exactly one company from that list survives in the top twenty: Exxon. Everything else had been replaced by U.S. software, R&D (pharma and semiconductor) and platform businesses.

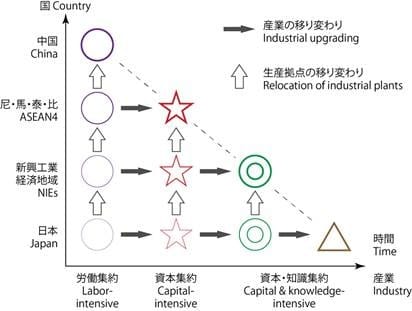

There’s a 1935 model from the Japanese economist Akamatsu Kaname called the Flying Geese:

The conception of a single developmental ladder, in which Japan would develop basic industries, move up the value chain, and then pass industries down to Korea and Taiwan, which would in turn pass them down to the next tier of developing economies, was elegant on paper.

Textile factories were layered by steel factories, and steel factories were layered with electronics factories, and skyscrapers would sprout concurrently from the substrate to house highly paid professional knowledge workers in high-value professional services and technology. The geese would fly in formation with parity with the West at the end of it.

These ideas and others like it were highly influential across developmental economics and industrial policy circles. An ascending ladder was enticing as an easily grokkable blueprint that also lined up well with GDP as a measure of national development.

The reality is that Japan, the Four Asian Tigers, and China didn’t climb a single ladder with incremental rungs from “low tech” to “high tech.” They climbed into a particular capability stack: process discipline, supplier coordination, capex deployment, time-to-volume. Those are technological capabilities. They are not the only technological capabilities.

That stack was particularly poorly suited to the software-platform era. The same institutions that produced flawless manufacturing discouraged labor mobility, entrepreneurial risk taking, immigrant recombination, and struggled at the kind of narrative-driven marketing that turns a product into a cult.

The ladder East Asia climbed was never a ladder into advanced technology in general. It was a ladder into a particular form of advanced technology: disciplined production at scale.

Those same competencies are why Asian cities feel "futuristic" to visitors from the West. The trains run on time to the second, the convenience stores are stocked efficiently, the streets are clean, the construction crews finish on schedule. None of this is magic – it is the same institutional muscle that built the supply chains, applied to the city itself. The future people imagined when they imagined "the future" looks the way it does in Tokyo and Seoul and Shenzhen because somebody had to actually build it, and the institutions that build things are concentrated in the part of the world that spent the last seventy years getting good at building things.

Two leaps

That being said, one of the particularly egregious challenges of building competencies as a manufacturing-focused economy into one that can build internet companies is that there are two leaps, rather than just one.

Ben Thompson’s Aggregation Theory, explained briefly is: the internet collapsed distribution costs to roughly zero, which meant the most important companies became the ones that owned the user relationship and made suppliers compete for access.

The first leap is learning to talk to end users – brand, taste, marketing, design. The second is learning to build network effects, developer ecosystems, and the corporate appetite to make messy bets on businesses that don’t make sense yet.

Each leap is its own institutional transformation. Even succeeding and becoming world-class at the first does not automatically net you the second. A number of world-class tech companies in Asia have struggled with one or the other – HTC, for instance (remember them?) seemed to get stuck on the first, and Sony and Samsung, on the second. These are instructive examples.

HTC was formerly an ODM best known for building the first Android phone – built several excellent devices and briefly became the largest smartphone vendor in the U.S. in 2011. It, however, was never quite able to build an appealing consumer-oriented brand that connected well with the mainstream. This gap was typified by a remarkably confusing $1 billion marketing campaign launched in 2013 starring Robert Downey Jr.

The centerpiece ad featured Downey nonsensically riffing on what HTC could stand for: “Humongous Tinfoil Catamaran,” “Hipster Troll Carwash," maybe “Hold This Cat” and then ending with a banger ending line that it was a “Happy Telephone Company.”

A good number of comments on YouTube — even in Taiwan — expressed confusion over what it was supposed to mean. HTC's ODM-to-brand transition worked for a brief window around 2011 when "competent Android hardware" was enough to differentiate — and collapsed once smartphones became an ecosystem game.

Sony built a catalog of beautifully engineered objects that made a generation of Xennials/Millennials gush about Japanese electronics with nostalgia and fondness usually reserved for childhood pets. Samsung’s 2010s were a clinic in catch-up: memory, displays, OLED, smartphones, capex on a national scale, fast-following Apple, competing on specs and price.

Both companies studied their global competition closely and made the leap to consumer brands. Unfortunately, neither quite succeeded at making the platform leap. Sony never managed to turn its empire into a coherently integrated consumer platform throughout the 2000s and 2010s, despite its incredible assets including PlayStation, Sony Pictures, Xperia smartphones, Alpha cameras, and VAIO laptops.

There were valiant attempts to build across segments and fulfill the vision of merging their hardware prowess with the emerging internet – the Digital Dream Kids initiative, for one – but organizational silos mostly stymied the efforts and led to internal competition – for instance when Sony Computer Entertainment’s 2003 ambitious PSX PlayStation 2/DVR hybrid ended up competing with Sony’s own video division products.

As for Samsung, Bixby, Tizen, SmartThings, and Samsung Pay also never became the organizing center of digital life for very many, despite their success in establishing themselves as a leading consumer brand and peer to Apple at their peak.

Hardware excellence isn’t consumer brand power, and consumer brand power doesn’t mean that a company will be proficient at building a platform. The second leap is harder than the first, and even Asia’s greatest consumer companies have had to discover this empirically.

The effect of legacy capabilities and structures shows up in B2B software too. In many parts of Asia, enterprise software did not quite become a clean, self-contained product category in the Silicon Valley sense. It was routed through system integrators, procurement departments, incumbent vendors, custom implementation projects, and a whole layer of people whose job was to make software conform to the company, rather than make the company conform to the software.

Customers often do not want an opinionated product that forces changes to well-established processes – many just want a vendor who can bend the tool around existing workflows, existing hierarchies, existing approval chains, and all the organizational sediment that had built up over decades.

In the manufacturing context, this is rational: buyers got customization, political safety, and someone to blame when things broke. Vendors learned to sell implementation, integration, and headcount-heavy delivery rather than scalable software products.

The exit environment for startups compounds the problem further: whereas Silicon Valley has native software giants with the balance sheets, product cultures, and strategic appetite to acquire young software companies, in much of Asia, that acquirer universe is simply much thinner and less accustomed to buying young software companies, with less ability to succeed at post-merger integration.

And underneath all of this sat a deeper macro legacy: when people are abundant and relatively cheap, managers reach for people before they reach for software. Spreadsheets, staffing agencies, the outsourced operations team, the system integrator, the junior employee quietly reconciling paper processes with company databases by hand – often become the default automation layer.

The factory at the frontier

This last two decades of tech and venture financing firmly established software businesses and the people who build them as the top of the hierarchy and, for many investors, the only really investable category.

I was reminded of this recently at a panel discussion in Tokyo featuring an impressive ex-Apple Chinese hardware founder working on a leading smartglasses product. Before starting his company in Shenzhen, he had spent years at Apple working on the Apple Watch before doing a few tours of duty at Chinese consumer hardware manufacturers.

At one point, he mentioned how hard it was to get a hardware startup off the ground in Silicon Valley – he likened pitching VCs on hardware to pitching a boba tea chain to tech investors – people were polite, but it was simply irrelevant to them because the business model was so fundamentally unattractive compared to software.

On the other hand, he found it extremely difficult to drive internal innovation into unproven white space internally at Chinese hardware giants despite their incredible capabilities and talent. Organizationally, they were structured to execute on a fast follower strategy to reverse engineer and outcompete Apple on price or product features or both. This was institutional: there wasn't even a mechanism internally to initiate an effort to build a category creating product.

This anecdote speaks to the challenges facing both sides of the Pacific: neither side, on its own, is well set up to drive the kind of innovation this new era demands.

However, this also means the map for innovation and innovation financing is changing. Batteries, EVs, solar, robotics hardware, defense production, shipbuilding, and industrial AI have always looked very different from software markets, with the added inconvenience of working in the real world making them second-class citizens in the U.S.

However, with this shift, the investable space is shifting to AI-boom-related programmable physical systems – production systems whose value increasingly comes from software, data, automation, reliability, and coordination, but whose value cap is set by physics, permitting, supply chains, and heat.

The thesis isn’t just investing in hardware – repeating some adage about how atoms are now eating software or something is its own trap since the fundamental economics haven’t shifted. The interesting question is which hardware ventures have become a part of the stack, and for whom programmability is still a story on a PowerPoint deck.

Dan Wang’s engineering-state frame in Breakneck exhorts the U.S. to rebuild its industrial base to be able to have a little more leverage.

“The US used to be more of an engineering state — it’s certainly built a lot. We’re chatting in New York City right now, and this is the city that built subway stations about 120 years ago. The United States built canal systems and highways and transcontinental rail systems and the Apollo missions, as well as the Manhattan Project. A lot of what I’m trying to do is to say that the US should recover some of these engineering muscles. It certainly doesn’t have to be like China. — Dan Wang, interviewed by WIRED

Incentives drive outcomes, and unless the incentives change substantially – and not just through the federal government putting a thumb on the scale via industrial policy – rebuilding the U.S.’s manufacturing base will be a fight against the conditions that led to the massive aggregation of capital and talent into software.

Of my class of 50-odd classmates who grew up mostly with parents working in the semiconductor industry in Taiwan who now reside in the U.S., I can count exactly zero who pursued a career in semiconductors or any sort of manufacturing. How many graduates of elite universities in the U.S. are dreaming of starting their careers on a production line or cleanroom, the same way that more than 8000 Taiwanese master’s and PhD students will this year?

The question now is whether headline drawing technological innovation looks more like the SF Bay Area or more like TSMC. Which is the real Silicon Valley of the next 30 years? This time, it is looking like it may be both.

Back to the future

All of which leaves one last question hanging in the air: is venture capital, in its current form, even the right vehicle for the next era?

It is easy to forget how recent the software-VC marriage actually is. The first venture firms in the United States were not built to fund consumer apps – they were built to fund semiconductors.

The shift to asset-light, high-margin, network-effects software was an adaptation, not the original mandate. Software’s capital efficiency, distribution economics, and exit dynamics happened to fit a particular institutional form – ten-year fund cycles, GP/LP structures, follow-on rounds compounding on early signal – extraordinarily well. Well enough that within a generation, “venture-backed” came to mean “software company” by default, and the deep-tech origins of the industry slipped into keynotes but rarely driving actual theses.

Companies building advanced packaging capacity, battery gigafactories, robotics platforms, fusion reactors, or AI infrastructure don’t look anything like SaaS. They need ten-figure capex before revenue, multi-decade payback periods, government coordination on permitting and grid interconnection, and demanding industrial customers who buy on specs.

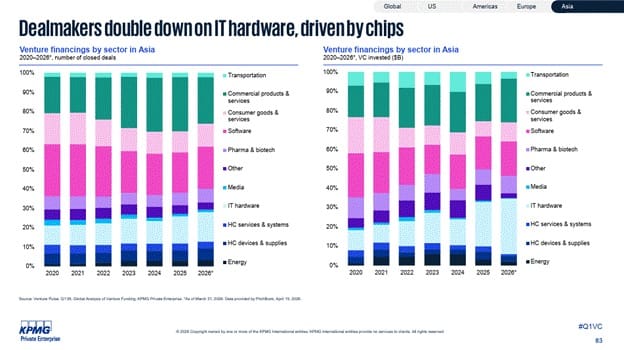

The structure is now visibly shifting in venture capital as well – KPMG’s Q1 2026 Venture Pulse showed Asian VC rebounding to $31.8 billion, with AI, semiconductors, and infrastructure taking the largest share – but with government and corporate capital playing an outsized role in the largest deals. The shift to hardware financing in Asia as a greater proportion of VC has outpaced shifts elsewhere.

This looks less like a return to the 2021 startup party than a gradual reallocation toward places where industrial capability, strategic capital, and technical bottlenecks are stacked on top of each other. It also looks a lot like the pre-software venture model Arthur Rock would recognize: longer-duration capital, strategic LPs with subject-matter expertise, and government as anchor customer and co-investor.

The process discipline and knowledge, the ability to deploy capex effectively, the supplier networks, the willingness to do unglamorous work at scale are an inheritance that just might perhaps shift the balance of those unicorn league tables – for the first time – towards East. This will take innovations and changes in venture – from due diligence and exit expectations, to the sorts of LPs cutting the checks to potentially different sorts of GPs.

As for the Silicon Valley – the San Francisco Bay Area version – a big question to answer is which capabilities – despite the uphill battle – to try to build inside the U.S. and which ones to work with partners, likely in Asia, to develop. This next wave of technological innovation is poised to leap into the physical world. The data centers and power plants are just the beginning.