05.31.2026

Chinoiserie Weekly: May 15-31, 2026

The Buyer(s) of Last Resort

Field Note

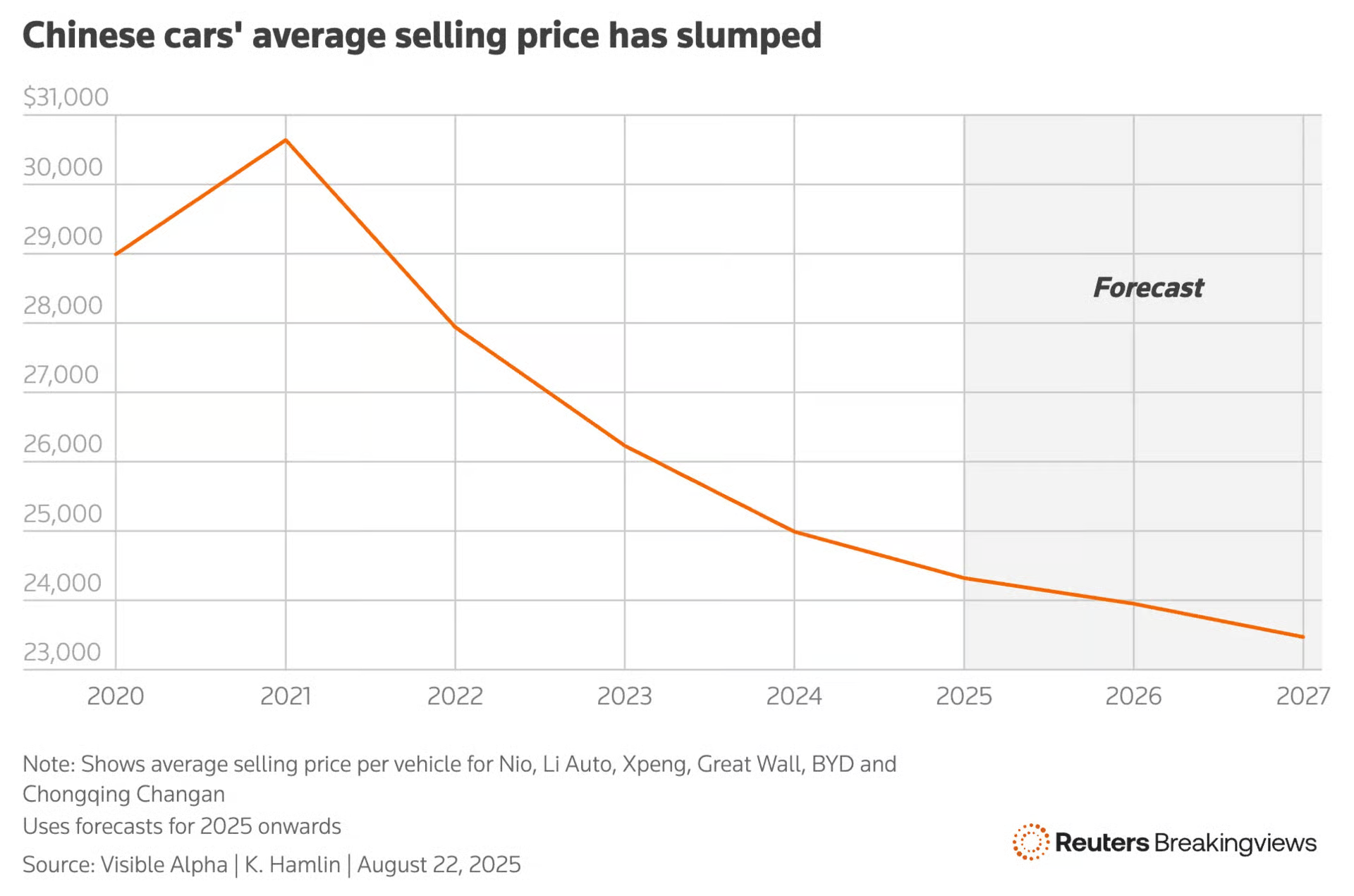

One of the most straightforward ways to understand China's economy right now is to watch the price of a car.

In the first quarter, Chinese passenger-vehicle exports rose 60.6% year-on-year, even while domestic auto sales fell 9.1%. The factories didn't slow down and the cars had to go somewhere, so they pointed the surplus outward exporting a price war that Beijing itself has spent the past year trying to end. The anti-involution campaign (反内卷) has as of date failed to stop the ruinous undercutting that has crushed profit margins.

In April, China posted a record monthly export haul of $359.44 billion USD, up 14.1% and the strongest showing on record despite tariff headwinds. But these goods are leaving for foreign markets because there is not enough demand inside China to absorb them; retail sales grew a thin 1.7%, a fraction of export growth. Consumer-goods prices also fell 1.0% year-on-year.

In Europe, Brussels has stopped treating the influx of manufactured goods as more than a grievance to be aired and have started treating it as a problem to tackled head on. This week, the NYT went as far as to blare a warning that Europe was edging closer to a trade war with China. As such, China's trade imbalance sits at the center of the European Commission's May 29 agenda, where five member states - Spain, Italy, the Netherlands, France, and Lithuania - are pressing for a new "overcapacity instrument" to drive enforcement.

Similarly, India, Brazil, and Argentina have all raised barriers against the Chinese goods flooding their market, despite being theoretically more friendly environments than prickly Western governments. As with their European counterparts, half of BRICS (and their friends) are discovering that a wall of subsidized imports does to a domestic manufacturing base in São Paulo exactly what it does to one in Stuttgart.

The one exception to this has been Southeast Asia - in large part because, unlike the others, Chinese imports might actually bolster local industry. This might come as a surprise to some, but ASEAN passed the EU and the US in 2020 to become China's largest trading partner, and trade across it grew another 15.7% in the first four months of the year, partly driven by "passthrough trade," where intermediate Chinese parts are reassembled in Vietnam and Thailand to be shipped off to Western buyers.

Economists at Harvard, Duke, and Academia Sinica reckon more than $8 billion of Chinese goods were passed through Vietnam alone in the first three quarters of last year, and the American deficit with Vietnam swelled by some $20 billion over 2025, to nearly $146 billion. Washington has noticed. Its deal with Hanoi keeps a 20% tariff on Vietnamese goods but threatens 40% on anything judged to be merely passing through.

Ultimately, the cure for overcapacity is domestic demand: money in households' hands, citizens buying what the factories produce, and an economy driven a little more by domestic consumption. Beijing's own economists have been saying so for fifteen years, and 2026 was billed as the year it would finally happen. But rebalancing is slow and politically expensive, and it runs against every reflex of a system built to produce. Exporting the surplus is quick, and it keeps the factories - and the local officials whose careers ride on them - running another quarter.

This isn't just a story that's started with China, of course: it's a major issue that runs through every major exporting East Asian economy. As per The Economist, Japanese private consumption is 53% of output, and in South Korea and Taiwan it is close to a paltry 40% - far less than the advanced economy the average of 60%.

Unlike its neighbors, however, China might be too big for the rest of the world to accommodate.

Capital Signals

Deals worth reading past the headline for

Flipkart × Domestic capital markets — Pre-IPO round / redomicile — ~$2–2.5B — Walmart-controlled

Flipkart completed its move to re-domicile from Singapore to India in March and is now sounding out a $2–2.5 billion pre-IPO round from Goldman, JPMorgan, Citi, Axis, and Kotak ahead of a listing targeted for the fiscal year ending March 2027. Walmart, which owns roughly 80%, holds the final veto, and the last benchmark valuation was $36 billion.

Why it matters: There is more to the redomicile than tax advantages - India has spent two years making it both cheaper and reputationally expected for its largest startups to list at home rather than in New York or Singapore, and Flipkart was the original poster child for the offshore holding company. Its reversal is a sign that the center of gravity for Indian tech capital is shifting home.

Samsung × Vietnam — Greenfield investment — $1.5B — Chip-testing plant, Thai Nguyen

Samsung is building a $1.5 billion chip-packaging-and-testing plant (39 trillion dong) in Thai Nguyen province, about 60km north of Hanoi, with operations slated for November 2027 and a potential second factory that could push the total to $2.5 billion. Some 200 engineers are already on site, and the focus is legacy DRAM and NAND back-end work.

Why it matters: Southeast Asia is building significant capabilities in the packaging and testing - the critical, but less glamorous - end of the chip business even while front-end fabrication stays locked up in Korea and Taiwan. Vietnam won't get a fab out of this, but it gets something that lasts longer: a steady foothold in a critical supply chain

Nvidia × Taiwan — Annual procurement commitment — ~$150B/yr — Supplier ecosystem + Constellation HQ

Jensen Huang said Nvidia will spend up to $150 billion a year with its Taiwanese suppliers and broke ground on its new "Constellation" campus in Taipei. The figure spans TSMC, Foxconn, Quanta, Wiwynn, and the long tail of component makers.

Why it matters: Spending on this scale ties Nvidia to a place, not just a set of suppliers. Every dollar of it deepens the dependency that makes the Taiwan Strait the most expensive stretch of water on earth, and cuts against every friendshoring pledge about diversifying away from the island.

Unitree × Shanghai STAR Market — IPO — ~$610M target — ~$6.2B valuation

Robotics maker Unitree is fast-tracking a Shanghai STAR listing at a target valuation around $6.2 billion, with a review scheduled for June 1. FY2025 revenue hit ¥1.71 billion (+335%), net profit roughly ¥600 million (about eight times the prior year), with humanoids now 51.5% of revenue.

Why it matters: Unitree is the rare Chinese hardware story where the growth is real and the foreign demand is genuine rather than dumped. The choice of venue says the rest: STAR rather than Nasdaq, a deliberate showcase for China's domestic capital markets at a moment when overseas listings have turned politically radioactive.

Backchannel Whispers

While Singapore's been in the news for being a model student (teacher?) with forward thinking investments and the launch of OpenAI for Singapore andNanoClaw-building Foreign Ministers, it hasn't been immune to the waves of tech layoffs over the last several years. There's also been a dramatic decline in the amount of venture capital - down 80% since the peak - deployed in the region to levels not seen since 2016.

At least some of these numbers this quarter will be from Palantir bucket hats sold at a standing-room only meetup with Alex Karp hanging out with us hoi polloi of Tokyo.

The Question of the Week

Enterprise software across Asia has often lagged the U.S. due to because fragmented distribution, relationship-driven business practices in legacy industries, and market-by-market localization needs. Will AI be different, or will the frontier labs’ blitzscaling playbook and on-the-ground revenue push crowd out the local application layer before it has a chance to form?

Additional Good Reads

- Nikkei Asia - In Asia, geopolitics has moved onto the deal sheet

- Nikkei Asia - Turkey sees 'strong potential' for drone development with Japan

- Nikkei Asia - SoftBank plans $88bn AI data hub in France as it expands beyond US

- Asia Tech Review - ByteDance hikes its AI spending to $70 billion in 2026

- Substack/Jostein Hauge - This is why I’m Chinamaxxing

- Substack/Hatone - The Silicon Valley "Inshu-Mura(因習村)": A Due Diligence Guide to Japanese Startups

- Reuters - Kyle Su's Kuark Capital launches $400 million Asia tech-focused hedge fund